Collaboration Avenues: Bridging the anti-money laundering and conservation communities to better address conservation crime and corruption

By

-

Judy Deane

This is the second in a two-part blog post series that distills learning from four 2021 roundtables convened under the TNRC project with leadership from TraCCC. These roundtables virtually connected a group of anti-money laundering (AML) professionals in the Washington, DC area with select conservation practitioners to seek touchpoints, identify information gaps, and future ways forward. As outlined in Part I of this blog post series, conservation practitioners and donors who integrate follow-the-money (FTM) approaches into their programming to address the impacts of crime and corruption on natural resources may get better results if they continue to strengthen collaboration with professionals in the AML community.

There is a wealth of data--some collected by conservation organizations, some held in financial sector institutions—that can offer clues and evidence about criminal activity and corruption in the environmental sector. But how do we put it together? How do we get stakeholders on the same page so that they can recognize the risks and connect clues in a way that results in actionable intelligence for law enforcement and/or action from governments? In our first 2021 TNRC roundtable in this series, conservation and AML experts came together to discuss how AML tools can be applied to address environmental crime and corruption. Our second and third roundtables focused on information, and our fourth on next steps for advancing cooperation between the conservation and AML communities. Key elements of our final three discussions are captured below as a guide for future work in this space by the conservation community and financial institutions.

Channeling the right information to financial institutions

In order to achieve desired results in targeting natural resource crime and corruption, information must be presented differently to different institutions. In general terms, the AML community needs to learn more about the importance of environmental crime, corruption, and destruction of biodiversity, so that they can better identify suspicious transactions in this sector. This educational effort is currently underway in the form of e-courses and other training materials, but more needs to be done. TRAFFIC’s recent Case Digest: Initial Analysis of the Financial Flows and Payment Mechanisms behind Wildlife and Forest Crime is an excellent case in point. It served as the centerpiece of our discussion in the third and fourth roundtables in this series.

The conservation community needs to learn how to best convey specific detailed information to the institutions that can put it to use, in a pattern that builds out a wider network and provides the evidence needed for law enforcement to take action. There are still important gaps in our understanding of the differences between how conservation organizations and financial institutions operate, and their information needs. Two major themes stood out in our second and third sessions: touchpoints and patterns. These are explored further, below.

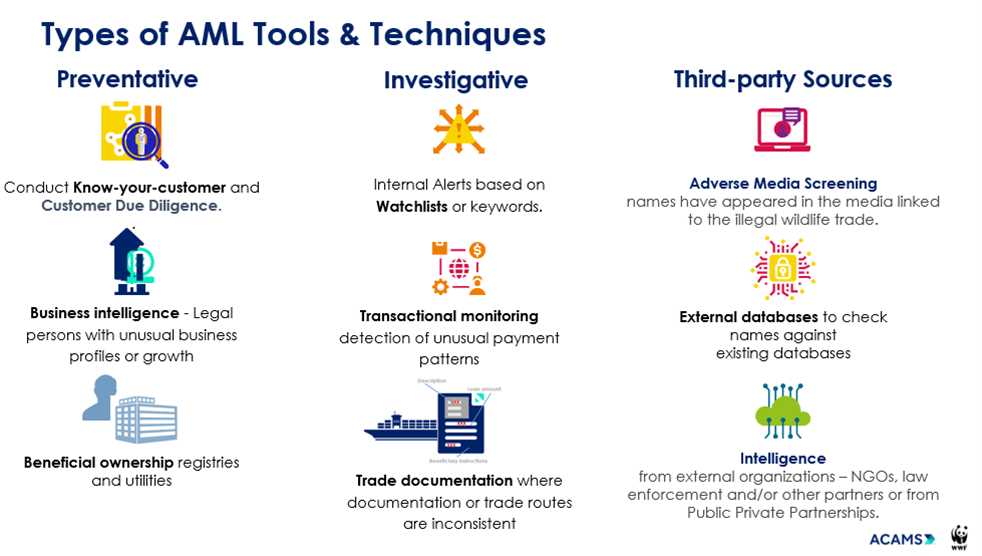

© Figure 1. Types of AML tools and techniques that can be leveraged to address illegal wildlife trade and corruption behind conservation crimes. Figure courtesy of ACAMS-WWF.

Understanding touchpoints

A touchpoint, in this context, is where a transaction that is linked to criminal activity touches a specific bank or other financial institution in a form that the institution can monitor. In all-cash or mobile money transactions, for instance, there are no touchpoints for banks to monitor. Payments that go through payment facilitators and some credit cards will not have touchpoints with major banks. However, like banks, these non-bank financial institutions have a responsibility to report suspicious transactions and have their own investigative teams who consider touchpoints with criminal activity in this sector. It is important to extend the dialog and educational efforts to reach them as well.

Banks are not all equal. There are local banks, regional banks, international, and 13 global banks. If the proceeds of illegality or corrupt practice are deposited into a local bank, and used for payments there, regional and international banks will have no visibility into the transaction. Even if the local bank had a correspondent relationship with an international bank, the latter would have no visibility into that transaction or reason to question it. Banks process a huge number of transactions on a daily basis. Wells Fargo, for instance, has 5,500 branches and 70 million customers. So the Know Your Customer (KYC) due diligence process and monitoring (see Figure 1) is highly automated. This brings us to the second theme that emerged in our discussion: patterns.

Identifying patterns

When a new customer comes into a bank to open an account, the bank collects some basic information, and checks personal identification, but does not verify the other information collected, except in unusual circumstances. Large international banks have their own investigative departments, sometimes running into hundreds of investigators. But even at large banks, the majority of KYC information comes from automated transaction monitoring. As a result, banks are generally reactive, rather than proactive, when it comes to information. They do not actively monitor wire transfers in real time unless some pattern of activity triggers an alert.

So what patterns of activity trigger alerts? There are patterns that are common to other illegal activity, but there also may be some that are unique to wildlife trafficking, or other environmental crime and corruption, that could be identified. Specific patterns of activity have been identified for human trafficking, for instance, that trigger alerts that help banks identify these transactions as suspicious.

International banks do additional monitoring based on risk factors. When a bank identifies a high-risk location for a specific illicit trade, such as the United Arab Emirates (UAE), for instance, it might review all the wire transfers from UAE for a month to look for a pattern of suspicious activities. Banks are sometimes alerted to risk factors through “negative news” such as newspaper articles about crimes, but most commonly they rely on third party vendors, who research and package “negative news” for them in line with bank profiles and their specific areas of interest. A pattern could present via repeated time or amount transactions, or by way of text in memo lines of wire transfer documents, for example.

How can conservation organizations best transform knowledge about environmental crime and corruption into usable risk alerts for banks?

How targeted does information have to be to trigger an alert? How can conservation organizations best transform knowledge about environmental crime and corruption into usable risk alerts for banks? Here are some immediate avenues for future cooperation discussed in our fourth roundtable:

- Build on latest efforts to examine financial data from wildlife crime cases and refine specific recommendations for local, regional, and international banks: Consider assembling a smaller group, including bankers, to go through recent analyses (such as TRAFFIC’s Case Digest that compiled detailed information from participating government agencies, financial intelligence units, non-governmental organizations and other sector experts) to further target some of the recommendations for financial institutions. Consider including a separation of recommendations for local/regional banks and international ones.

- Expand the participants in this dialog to include more representatives from banks, other financial institutions and payment facilitators: Consider involving nonbank financial institutions since many of the illicit payments go through their payment systems.

- Further explore whether third-party vendors who package “negative news” for banks’ adverse media screening systems sufficiently consider news about environmental crime and corruption: If not, engage them further.

- Work further with FinCen, FATF, and/or the Egmont Group to develop more targeted alerts on environmental crime and corruption.

- Develop “test” cases to see how trade discrepancy analysis (TDA) can generate meaningful patterns for banks’ intelligence systems: For example, consider specific natural resource commodity export routes where a significant proportion of the trade is illegal, and perform a TDA, using Comtrade plus a commercial trade database that provides detailed info on vessels, import firms, exporters, etc. See whether this provides sufficient information to develop meaningful patterns and alerts that can be used to develop actionable intelligence, and if so, what kind of information is most useful.

There’s much to do. The financial and conservation communities will need to continue to develop stronger partnerships and work in tandem in future years to address natural resource crime and corruption.

In November 2022, TRAFFIC released a series of good practices for communicating with the finance sector to combat corruption that is linked to illegal wildlife trade and money laundering. Those good practices are available here.

This content is made possible by the generous support of the American people through the United States Agency for International Development (USAID). The contents are the responsibility of World Wildlife Fund (WWF) and do not necessarily reflect the views of USAID, the United States Government, or individual TNRC consortium members.